#1 The Kelly Criterion Explained!

Sizing your next trade made simple!

Have you ever wondered how much of your capital should you deploy for the next trade? Is there any magical formula that could come to your rescue? Well, there is one, and we discuss that in our first post, and there is a high probability that you may not have come across the same even in the programs like CFA or MBA. Your interest would skyrocket if we tell you that it is used by the most celebrated investor Warren Buffett, his friend Charlie Munger, and Edward Thorp (he had come up with, and profited from an equation in 1969 that was similar to the Black Scholes Equation, which was published in 1973, just in case you didn’t know the guy).

The equation, soon to be decoded, was developed by John L. Kelly, Jr., in 1956, while working for AT&T’s Bell Laboratories. The equation was later picked up by horse racing gamblers, blackjack players, and other bettors, before finding its way to the capital markets.

Now, let’s cut to the chase. To decide how much of the capital should be deployed in your next trade, you could either listen to your gut, or use the Kelly Criterion to come up with a number.

If you are a math-head, like us, and decide to use the Kelly Criterion, there are several things you need. First of all, you need to have been trading using a certain set of measures and need to have some data of the previous trades. These previous trades will help you get the probability (based on the number of profitable trades out of the total trades) and the win ratio (total amount of profit ÷ total amount of loss). Take the probability and the win ratio to put them in this equation:

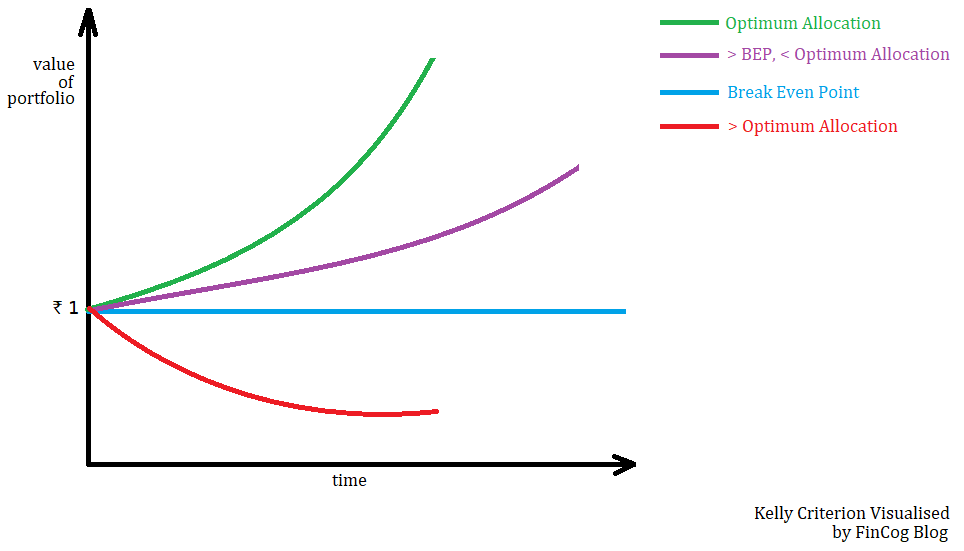

Let’s say, out of your last 50 trades, 26 trades turned out to be profitable i.e. in 52% of trades you made profits, so, 52% will be the probability of winning in the equation. And let’s say, out of those 50 trades, you made INR 11,000 in 26 trades and lost INR 10,000 in 24 trades, so, you get a win ratio of 1.1 i.e. 11000 ÷10000. Now, according to the Kelly Criterion, you should deploy approx. 8% (8.36%, to be precise) of your capital in the next trade. What happens if you deviate from the optimum allocation of 8%? If you deploy more than 8%, the results would be amplified, but that is a double-edged sword that could potentially wipe out the entire capital (the red curve in the graph). And if you deploy less than the optimum number, then it would quieten the magnitude of the returns (the purple or the blue curve in the graph).

When it comes to having limitations, the Kelly Criterion, just like almost every other mathematical model in finance, ignores transaction costs, taxes, etc. The model is still subject to human judgement about capital allocation, and self-constraints.

So, next time when you hear Kelly Criterion, make sure you say: the criterion recommends deploying a fraction of the trader’s capital proportional to the expected return of each trade.

Did you enjoy reading this? Do let us know. If you have any suggestions or if you would like us to cover any particular topic, reach out to us at finance.cognoscenti@gmail.com. We would love to hear from you.

Stay tuned for upcoming posts. Please subscribe and don’t forget sharing is caring.

Stay home! Stay safe! Practice social distancing!

Until next time…

You can connect with us on LinkedIn at Hind & Punit and follow us on Twitter at @hindpansuriya and @punit_pujara.